With 2016 almost at a close the analysts and economists are commenting on what they expect the New Year to bring in investment markets. We have prepared the following blog post based on commentary from Chief Economist Dr Shane Oliver at AMP Capital Investors and the Research Team at Vanguard.

With 2016 almost at a close the analysts and economists are commenting on what they expect the New Year to bring in investment markets. We have prepared the following blog post based on commentary from Chief Economist Dr Shane Oliver at AMP Capital Investors and the Research Team at Vanguard.

Dr Share Oliver Comments:

- 2016 started badly for investors with worries about global growth and deflation. But global growth turned out okay &, despite political events, rising bond yields & disappointing Australian growth, the end result has been a constrained but okay year for diversified investors.

- 2017 is likely to see another year of okay & maybe even slightly higher global growth, higher inflation, higher bond yields after a pause and divergent monetary conditions as the Fed tightens but other countries stay easy. The RBA is likely to cut rates to 1.25%.

- Most growth assets, including shares are likely to trend higher, resulting in reasonable returns in 2017.

- The main things to keep an eye on are US policy under Trump (stimulus v trade wars), the Fed and the $US, bond yields, various European elections, China and the impact of the rising supply of apartments in Australia.

Global economy: Stabilisation, not stagnation

Since the end of the Global Financial Crisis, economic growth has fallen short of historical averages and consistently disappointed policymakers. Deflationary shocks have roiled the markets, and much of the world’s bond market offers negative yields. Some analysts still believe the world is headed for Japanese-style secular stagnation. And yet the modest global recovery—at times frustratingly weak—has endured, proving the most ardent pessimists wrong.

Monetary policy and interest rates: Central banks grapple with their limits

The U.S. Federal Reserve is likely to pursue a “dovish tightening,” raising rates to 1.5% in 2017 while leaving the federal funds rate below 2% through at least 2018.

Elsewhere, further monetary stimulus seems possible, but its benefits may be waning and, in the case of negative interest rates, potentially harmful to the very same credit-transmission channel that monetary policy attempts to stimulate. Even so, the European Central Bank (ECB) and Bank of Japan (BoJ) could yet add to the quantitative easing implemented in 2016.

Domestically, the Reserve Bank of Australia (RBA) is expected to adopt a neutral stance. However, we are hesitant to call the bottom of the easing cycle, given the risks associated with inflation, the peak in construction activity and rising global trade frictions.

Investment outlook: Muted, but positive given low-rate reality

Vanguard’s outlook for global stocks and bonds remains the most guarded in ten years, given fairly high equity valuations and the low-interest-rate environment. We don’t expect global bond yields to increase materially from year-end 2016 levels.

Bonds. The return outlook for fixed income remains positive, yet muted. The expected long-run median return of the broad taxable fixed income market is centered in the 1%-3% range. It is important to note that we expect the diversification benefits of investment-grade fixed income in a balanced portfolio to persist under most scenarios. As we stated in 2015, even in a rising-rate environment, short duration tilts are not without risks, given global inflation dynamics and our expectations for monetary policy.

Stocks. After several years of suggesting that low economic growth need not equate with poor equity returns, our medium-run outlook for global equities remains guarded in the 6%–9% range. That said, our long-term outlook is not bearish and can even be viewed as a positive when adjusted for the low-rate environment.

Asset allocation. Vanguard’s outlook for portfolio returns is modest across all asset allocations when compared with the heady returns experienced since the depths of the Global Financial Crisis. This guarded but not bearish outlook is unlikely to change until we see a combination of higher short-term rates and more favorable valuation metrics. The investment environment for the next five years may prove more challenging than the previous five, underscoring the need for discipline, reasonable return expectations, and low-cost strategies.

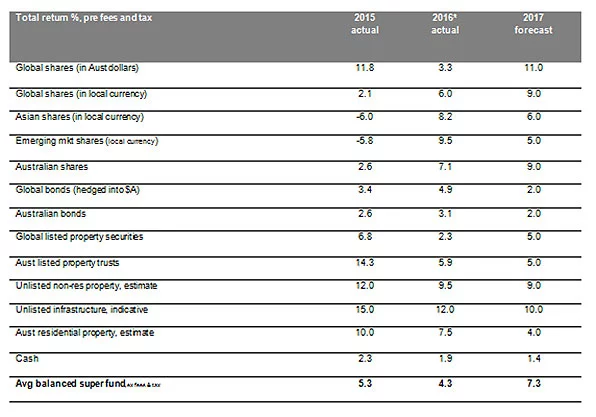

AMP Capital has prepared the following graph on what we should expect from each Assets Class in 2017

* Yr to date to Nov. Source: Thomson Reuters, Morningstar, REIA, AMP Capital

Dr Shane Oliver says that these are the main things to keep an eye on in 2017:

- US economic policy under President Trump – in particular whether the focus is on fiscal stimulus and deregulation as opposed to starting a trade war with China;

- How aggressively the Fed raises rates – faster inflation could speed it up putting more upwards pressure on the $US;

- A rapid rise in bond yields – this would be bad for shares and growth assets but a gradual rise would be okay;

- Elections in the Netherlands, France, Germany and maybe Italy which could reignite Eurozone break-up fears if anti-Euro populists win (which I doubt they will);

- Whether China continues to avoid a hard landing;

- Whether non-mining investment picks up in Australia – a failure to do so could see aggressive RBA easing – and how a surge in apartment supply impacts property prices; and

- Ongoing geopolitical flare ups, eg in the South China Sea.

For the full report from Vanguard see the following link.

For the full report from Dr Shane Oliver at AMPCapital click the following link.

Legg Mason Economic Update

Seek out further advice and start your journey to being free around your money and creating wealth with understanding.

Scott Malcolm has been awarded the internationally recognised Certified Financial Planner designation from the Financial Planning Association of Australia and is Director of Money Mechanics. Money Mechanics is a fee for service financial advice firm who partner with clients in Melbourne, Canberra and Sydney to achieve their life and wealth outcomes. We are authorised to provide financial advice through PATRON Financial Advice AFSL 307379.

The information provided on this article is of a general nature only. It has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information you should consider its appropriateness having regard to your own objectives, financial situation and needs.